{kind=link}

The large law firm service delivery model continues to evolve according to the just released Citi 2020 Client Advisory, prepared with Hildebrandt Consulting (PDF). I summarize key findings here on the service delivery model and comment on them. Citi writes

“we expect that firms will continue to develop more innovative service delivery models… With the growing competition from Big Four accounting firms and alternative lower cost service providers, we expect that law firms will focus even more so than before on delivering their services more efficiently.”

This supports my long-stated view that most commentators overstate the threat that alternative legal service providers will disrupt law firms, or even take sizable share from them. In my opinion, they fail to consider how large firms are changing and improving their service delivery model. The Citi report highlights multiple steps firms take to remain competitive, including more automation, project management, online subscriptions, and lower cost leveraged timekeepers.

Before examining a couple of these changes in detail, here’s a brief explanation of why the service delivery model has changed. The market remains very competitive and growth low. Citi found that large firm revenue grew 5%, with most of that increase coming from rate increases. Underlying demand grew less than 1%. In an almost flat market, competition for new business remains fierce so firms spend more to win a bigger share of the same pie.

Automation, Especially AI Use, Up Markedly in Two Years

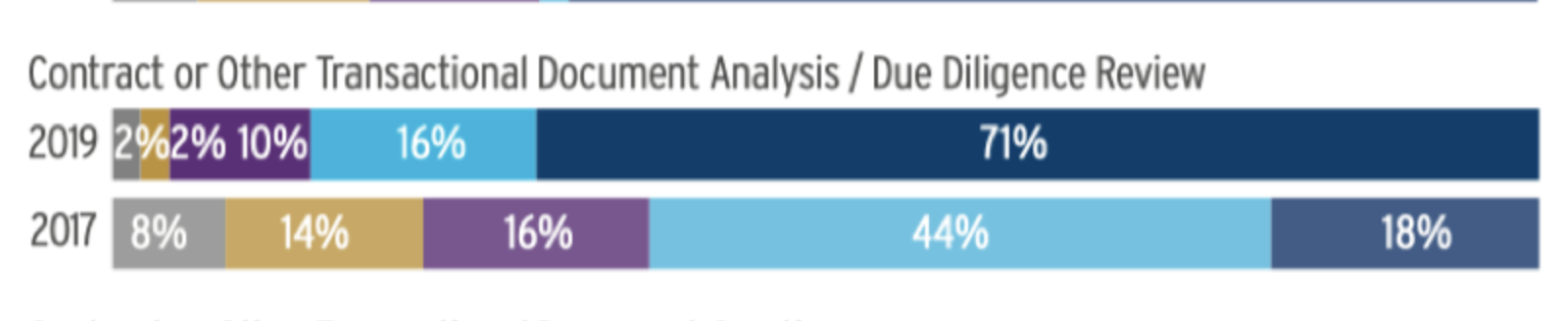

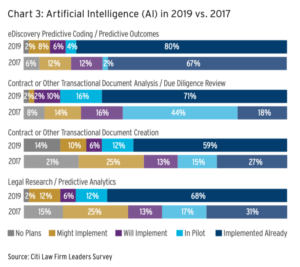

Law firms have adopted AI to deliver service more efficiently: Citi found a big jump in the use of artificial intelligence. I give more weight to Citi findings than to other surveys. Citi talks to many Am Law 200 firms, which share data more freely with Citi than they do with others. This chart, copied from the survey, speaks volumes:

Note especially these 2017 to 2019 jumps in AI usage:

- 4x increase in the number of firms using AI for due diligence reviews, from 18% to 71%

- 2x increase in document automation, from 27% to 59%

- 2x increase in use of third-party legal analytics tools from 31% to 68%.

What do these findings mean? On the one hand, these big jumps in the number of firms using AI does not tell us the extent to which lawyers in these firms use the tools. If a firm licenses a tool and only a few lawyers use it, the impact is limited. On the other hand, irrespective of individual lawyer uptake, alternative providers can no longer credibly claim they use more technology (or even use it better). At minimum, these findings force ALSP to support any claims they make about their use of AI.

More Non-Partner-Track Timekeepers Improve Value

Smart firms understand that a sure path to improve both client value and firm profit is utilizing larger numbers of lower cost timekeepers. For the same reason, ALSP emphasize their use of an overall lower cost mix of labor. The Citi report suggests law firms will act to level the playing field….

Three quarters of firms plan to add “permanent lower cost” timekeepers, which is the second fastest growth category after associates. This could include, for example, staff attorneys. And 45% plan to increase “other timekeepers”, which includes “eDiscovery personnel, specialist advisors, project managers, professional support lawyers, patent agents, technology professionals and law clerks.”

Of particular note is the growth in project managers:

“Just a few years ago, firms tended to focus on training partners and associates in project management skills, rather than hiring full time project managers. Now, we increasingly see clients who are willing to pay for this project management service in its own right, because it can help manage costs.”

In my view, boosting the ranks of lower cost lawyers and project managers signal that law firms understand client have lower cost alternatives. Firm management plans to compete head-on by adjusting the service delivery model.

Clients Remain the Rate Limiting Factor

Despite some noise from a few vocal General Counsels and some dire predictions of disruption, the data suggest – as they have for years – that clients are, in fact, not hurrying to change. The Citi report is for and about law firms but one finding reflects on clients, specifically concerning alternative fee arrangements…

“In 2018, just 17.2 percent of law firm revenue came from AFAs.” Alternative fee arrangements appear to be like teenage sex, much more discussed than actually practiced. The survey finds law firms offer AFA more often than clients accept them. “Law firms consistently tell us that, even when clients initially request an AFA, they often later revert to requesting a discounted hourly rate.” (emphasis added).

Conclusion

Since the 2008 economic crash, Citi has repeatedly sent a similar message: slow demand growth, fierce competition, and improvements in the service delivery model. In my view, the biggest change in the last 2 or 3 years has been the uptake of AI and investment in innovation (which Citi did not cover). When I read the 2025 Client Advisory, I hope it will show how the innovation emphasis starting pre-2020 converted to better, faster, and more cost-effective Big Law service and outcomes.