Two recent surveys, the Altman Weil 2017 Chief Legal Officer (CLO) Survey and the 2018 Report on the State of the Legal Market by The Center for the Study of the Legal Profession at the Georgetown University Law Center and Thomson Reuters Legal Executive Institute and Peer Monitor® provide a great snapshot of the state of the legal market.

I highlight here some findings from both, separated into law firms, law departments, and alternative legal service providers. My commentary appears intermixed with findings highlights but I also have offer two overarching comments:

- Client-Firm Missing Link. Altman Weil (AW) reports that clients find law firms wanting. Georgetown reports that law firms risk losing much if they don’t transform. We have read similar reports in the past. The missing link is what will it take to close the gap between what clients say they want and what law firms provide? One answer, in part, is changes to law firm compensation. And another answer, in part, is clients exercising buying power more clearly.

- Alternative Legal Service Providers Mystery Disconnect? Evidence exists in both reports – though it is mixed – that alternative legal service providers are gaining share from law firms. I can cherry pick data to support or undermine this claim. Read my assessment below for more.

Law Firm Perspective – Georgetown

- Law Firm Performance (Pages 2-3)

- The Georgetown report opens with a 2-page discussion about failures of strategy, starting with the famous Maginot Line and pivoting to recent research that explains why humans often double down on failing strategies (“consensual neglect”).

- It then applies that to large law firms, concluding

-

“This phenomenon of ‘consensual neglect’ seems a particularly apt description of the strategic posture of many (if not most) law firms in today’s rapidly changing market for legal services. Ignoring strong indicators that their old approaches – to managing legal work processes, pricing, leverage, staffing, project management, technology, and client relationships – are no longer working, they choose to double down on their current strategies rather than risking the change that would be required to respond effectively to evolving market conditions.”

- The report analyzes (pages 4-14) law firm financial performance over the last decade. Most indicators are down. Furthermore, averages conceal increasing divergence among subsets of the Am Law 100. And finally, Georgetown concludes that come next downturn, few firms will have many levers left to pull because all were pulled 10 years ago post-crisis.

- Desperation? These findings differ little from last year. Perhaps I am projecting, but I detect a sense of desperation in the report that law firms have yet to change how they work.

- What Can Be Done?

- Law firms must respond to “consistent client demands for greater efficiency, predictability, and cost effectiveness in the delivery of legal services.” Specifically, Georgetown finds that “Over the last few years, there has been mounting evidence that law firms that proactively address the needs of their clients – e.g., by implementing alternative staffing strategies, pursuing flexible pricing models, adopting work process changes, making better use of innovative technologies, and the like – can achieve significant success.” (Pages 16-17)

- Repetition is Conviction (or What of Compensation)? We’ve heard this message before as well. I do not mean that to be critical. Rather, it’s simply an observation of clear need with little execution. Unaddressed in either report are changes in compensation and buyer behavior required to drive change.

Law Departments – Altman Weil

- Efficiency Tactics (Pages 10 and 11)

- The AW survey asks “In the last 12 months, have you done any of the following to increase your law department’s efficiency in its delivery of legal services? (Check all that apply.)”

- Among law departments of 51 or more lawyers, 81% used tech tools more and 46% used knowledge management (KM) more.

- When asked about which of these tactics yield “significant improvements”, 59% rate tech as “yes” and 38% yes for KM. I don’t view the gaps between use and improve as that large.

- The three highest ranking improvement tactics in this questions are outsourcing to non-law firms at 74%, greater use of paralegals at 73%, and project staffing with contract or temp lawyers at 72%.

- Don’t Confuse Labor Cost Arbitrage and Efficiency. Efficiency (increasing output per hour) is not the same as reducing labor costs. The three top three ranked ones reduce labor cost via delegation to lower cost resources. In contrast, legal tech and KM, used appropriately, do increase output per hour. Both valuable but different.

- Cost Control (Pages 3 and 12)

- In response to “In the last 12 months, have you done any of the following to control law department costs? (Check all that apply.)”, the top answer was 64% for law firm discounts.

- Law departments still plan to add in-house lawyer, with 4.5x as many departments planning to add lawyer headcount versus decrease it.

- Continued Reluctance to Tackle Changing How Lawyers Work. I worry clients and firms play a cat and mouse game with rates and discounts instead of focusing on changing both how firm and department lawyers work. We need to see better scoping, higher efficiency, and improving service delivery. Bringing lawyers in-house is just another labor cost arbitrage move – it does not automatically improve how lawyers work.

- Law Firm Service Improvements (Page 37)

- When asked what service improvement and innovations they would most like to see from law firms, 51% of CLOs said greater cost reductions and 46% improved budgets. These are the top two answers.

- No Surprises Here. We have been hearing this message for years. Until both clients and firms focus more on changing how lawyers work, the answers likely won’t change.

Alternative Legal Service Providers

- Clients Say Outsourcing is Effective. CLOs say the most effective efficiency tactic is outsourcing to non-law firms (see AW Efficiency Tactics above).

- Georgetown Reports ALSP Revenue and Impact. The report has a lengthy discussion of the role of alternative legal service providers and asserts they are growing.

- ALSP Findings Are Inconsistent

- ALSP Least Understand Client Challenges. The AW Bonus Question this year (page 45) asks about “Understanding Law Department Challenges”, specifically “On average, how would you characterize each of the following stakeholders’ knowledge and understanding of the challenges of leading a law department?” The choices are non-law firm vendors, organization executives, and outside counsel. Non-law firm vendors score lowest.

- More GCs Say They Will Increase ALSP Spending. Georgetown cites AW for “for the first time since 2013, more law departments increased their vendor budgets than decreased them”

- ALSPs Are in News. Georgetown cites recent news: the United Lex deal to outsource a big chunk of the DXC law department and PwC launching a flex law service. Today, Deloitte in the UK announced today it will become an ABS to offer more legal services.

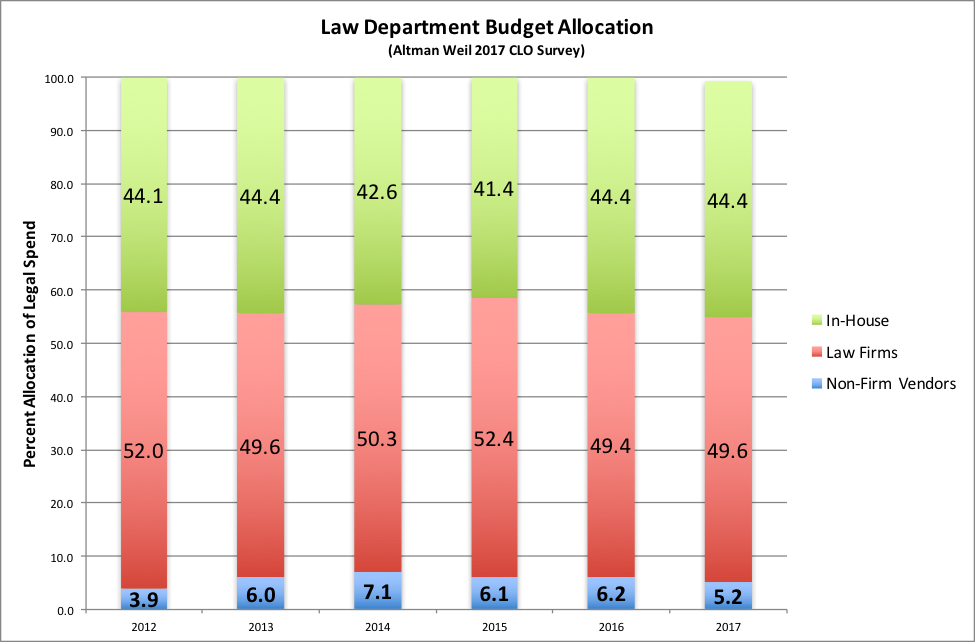

- YET, Time Series Data Speak Otherwise. Since 2013, AW asked (page 21) CLOs to estimate the percent of spend by internal, law firm, and non-law firm vendor. As the graph below illustrates, spending on non-firm vendors, which includes alternative legal service providers, remains in the mid single digits with a shrinking share since 2014.

- The Mystery. Many reports and commentators says ALSP is growing absolutely and taking share from law firms. Yet, the only time series data I have seen that asks about actual spending (not intent to spend) is what I graph below. So we have a mystery disconnect.